The Bridgetown Initiative – Fit to Finance Climate Justice?

Gaya Sriskanthan, Tetet Lauron, David WilliamsThe Genesis of the Bridgetown Initiative: Forged in The Fire of Barbados’ Debt Crisis

In 2018, after prolonged difficulties stemming from the 2008 financial crisis that served to heighten structural weaknesses in its national economy, Barbados suffered the fate that so many developing countries are currently struggling to avoid. Burdened with unsustainable levels of national debt, the country was forced to restructure its debt. Mia Mottley, the current Prime Minister of Barbados, had only just taken office at this time, steering the country out of one of the biggest economic challenges it had ever faced. Barbados is a small island state and deeply vulnerable to the climate crisis. This was factored into the restructuring, which uniquely embedded climate risks into its terms. Barbados was one of the early pioneers in this approach, repackaging existing debt into bonds that had built-in natural disaster clauses to automatically suspend debt payments for two years in the case of officially recognized disasters. This would provide needed respite in an emergency, though payments would resume after the two-year period, even if the country were still in economic difficulty.

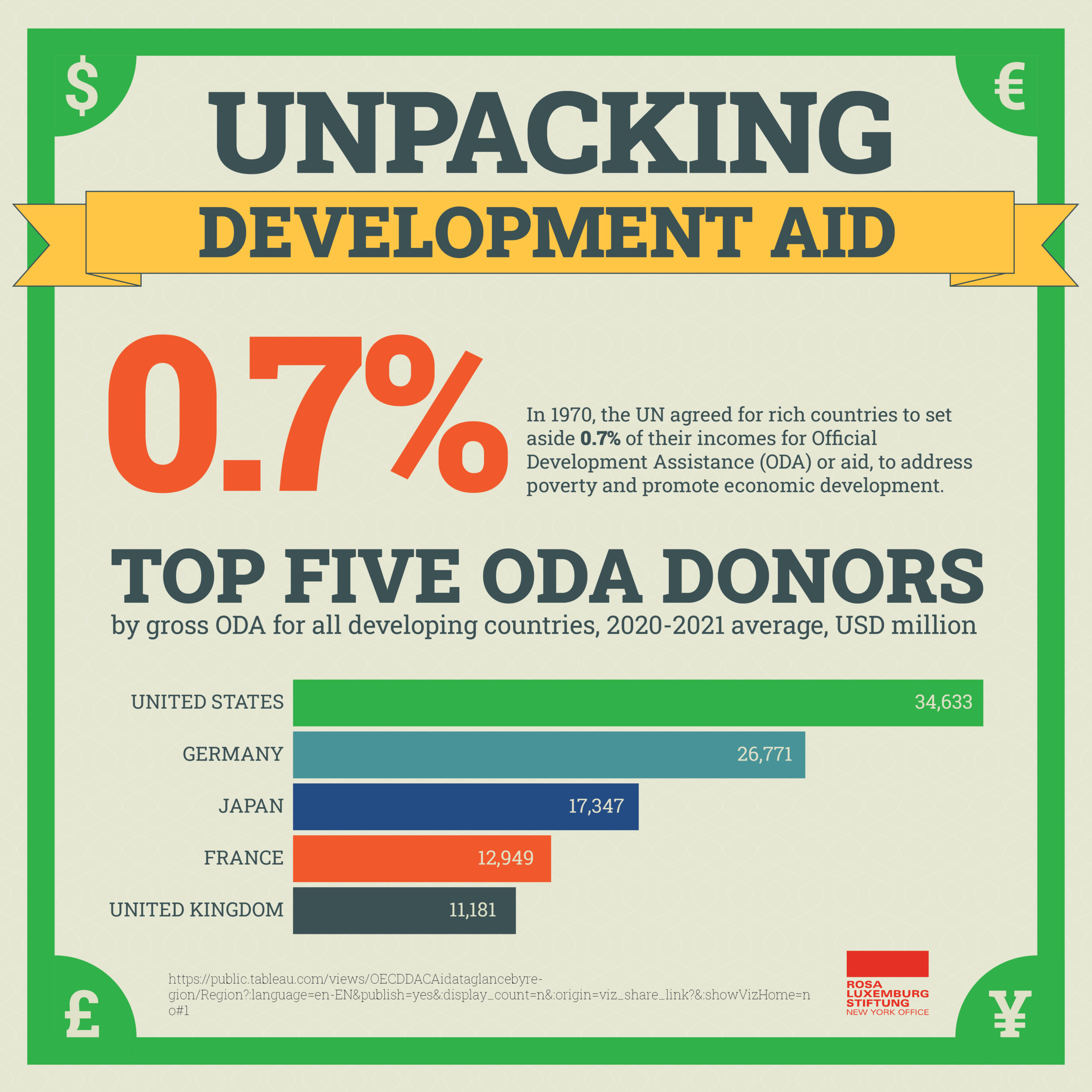

Mottley has since become an authoritative voice on the issue. At the United Nations (UN) climate talks in Glasgow in 2021 she spoke powerfully, drawing attention to the hypocrisy inherent in how rich countries had dealt with the domestic impacts of the pandemic by unlocking vast monetary resources. This contrasted with their failure to provide the levels of climate finance they are obligated to under the UN climate convention. In this speech she touched on the need to reform the way the international financial system operates and the way banks conduct lending, mentioning several available tools. These included the issuance of Special Drawing Rights (SDRs),[1] which were used during the pandemic and could be repurposed to support development and climate finance needs.

In the months that followed this speech, Mottley led further work with Avinash Persaud, the former leader of the Financial Services Commission of Barbados who served during the country’s debt restructuring period. She convened a high-level meeting in the country’s capital in July 2022. This gathered academics alongside representatives of the International Monetary Fund (IMF) and UN to hammer out ideas to address some of the continuing debt and climate finance problems facing developing countries. Dubbed the Bridgetown Initiative (BI), the one-page document that emerged from these discussions clearly integrated Barbados’s experiences in debt restructuring with other elements.

The initial proposal had three key components. The first dealt with a critical issue faced by developing countries contending with both development and climate needs: the ability to access to money quickly and easily, particularly in emergencies. The BI one-pager proposed a number of existing IMF tools that could be expanded or directed for this purpose. This included giving access to rapid credit and other forms of finance without constraining conditions. It also asked to re-channel existing unused SDRs that were allocated during the pandemic, to rapidly operationalize the IMF’s new Sustainability and Resilience Trust, and to suspend the widely condemned surcharges – which incur more costs on top of interest and debt repayment schedules- imposed by the IMF on countries unable to repay their loans quickly enough.

Secondly, it called for the expansion of lending from multilateral banks by US $1 trillion in a manner that prioritizes achieving the Sustainable Development Goals (SDGs) and building climate resilience. Thirdly, it demanded the creation of a global grant-making mechanism for any country’s reconstruction needs after a climate disaster, plus the issuance of low-interest, long-term financing to catalyze private sector investment in climate mitigation.

The Bridgetown Initiative is Influencing Climate Finance Debates, But What Are its Strengths and Limitations?

Barbados’s advocacy around this proposal culminated at the 27th UN climate talks (COP27), held in Egypt in November 2022. The BI was highly influential during these meetings. It contributed to the adoption of a decision under the UN climate convention to call for multilateral development bank (MDB) reform in order to align with climate financing needs. At the closing of COP27, President Macron of France announced he’d host a Summit for a New Global Financial Pact which would include discussion of the BI proposals in addition to questions of broader development financing.

It is remarkable and impressive that one page of text and deft diplomacy has sent such ripples through the climate and debt landscape, but we also need to look at the context. The BI comes at a time when MDBs are already under intense scrutiny. They are perceived to have failed to respond to the immediate economic crisis caused by the pandemic and its repercussions, as more countries plunge into debt distress. The iconic case of Pakistan highlights how climate disasters can intersect catastrophically with prevailing, unstable economic conditions.

There are growing demands for these institutions to be responsive. For instance, this year the World Bank – under pressure from its own member governments – launched its “Evolution Roadmap”. In foundational documents towards this, the Bank noted that the “world is facing crisis of development”. However, it has been critiqued for not going far enough in reforms to actually address the problem.

It is clear that international finance institutions (IFIs) want to become more central to climate financing. However, many of these institutions have a history of funding huge, extractivist projects with severe negative impacts on communities and the climate. The fact that they are in the process of reinventing themselves as climate champions without addressing their past has led to some suspicion. Additionally, structural adjustment programmes – packages of reforms forced on countries that often de-fund the public sector and sell off public assets – have contributed to making developing countries more vulnerable. In some ways the BI, particularly as a proposal generated in the global south, has contributed to filling a political vacuum in a number of different multilateral policy spaces. However, it is also bolstering the idea that the IFIs should be more central in solving climate finance problems.

But what are the full implications of its promise and reach? One difficulty in answering this is that the BI has become a moving target. From its beginnings as a concise, one-pager with three key pillars, foregrounding emergency liquidity and lending reforms, it has morphed over the months to expand and re-center its focus. By November 2022 the BI had been reshaped into five proposals that, at their core, put forward ideas for generating mitigation, adaptation, and loss and damage financing.

In pole position, the first proposal of this tweaked BI framework expanded on the idea of financing mitigation activities buried in the last pillar of the original one-pager. In this iteration, it was given clearer form as a Climate Mitigation Trust. Mitigation activities, such as the development of renewable energy projects or decarbonization of commercial agriculture, are more attractive for private finance given the possibility that an investment will yield returns. However, private investors can also be risk averse, particularly when it comes to investing in Global South countries – precisely where access to more finance for mitigation activities is needed. The original iteration of the Trust aimed to address this problem by using public money in the form of $500 billion in SDRs as a financial guarantee.

Private investment is hard to secure for adaptation projects as, unlike mitigation activities, they are unlikely to have a secure return on investment. Proposal two in this version sought to address this gap by expanding access to loans provided with friendlier terms, such as lower interest rates and longer repayment schedules, to finance adaptation activities.

Proposal three called for a $1 trillion increase in MDB lending, including concessional finance, again suggesting SDRs and donor guarantees to back this funding. Proposal four put forward the idea of a tax on fossil fuels to fund a $200bn per year grant mechanism for loss and damage. The final and fifth proposal revisited the original disaster clause for lending.

Civil society response to the meteoric reach of the BI’s influence has been nuanced. There has been appreciation for Barbados’s leadership on this issue and the attempt to force the need for financial systems reform into the spotlight in a way that acknowledges the need to address debt burdens in tandem with climate finance needs, as well as call for new climate financing streams through modalities such as innovative taxation.

However, some concerns have surfaced, as discussed by civil society in open fora such as the Civil Society Policy Forum at the margins of the World Bank and IMF Spring Meetings. One major worry is the move to over-rely on private sector finance that is also being reflected in the agendas of major IFIs. What is particularly concerning is that this has already been tried and failed to achieve the expected results under the World Bank’s “billions to trillions” agenda, which was aimed at trying to entice private investment in social development and climate action through the provision of complementary public funds. Additionally, the BI presents an agenda for increased dependence on lending for both mitigation and adaptation financing. This has alarmed some as it represents a further increase in debt burdens to take on climate challenges in addition to development goals, even if some of this debt is at concessional rates.

Perhaps partly in response to these brewing concerns, in April 2023 the UN Secretary General (UNSG) and Mottley convened a meeting to release a further iteration of the BI that marks a slight change of course. The Bridgetown Initiative 2.0 walked back the idea of a Climate Mitigation Trust, instead leaving the modality for a goal of $1.5 trillion per year of private sector investment in the green transformation open ended. It added an ask to restructure existing debt on more favorable terms and demanded a fairer international trade system consistent with just, climate action

One gap in the current BI 2.0 as well as the older versions, is that it doesn’t specify where any of the newly proposed modalities should be housed and how they should be governed. Inherent in the BI’s proposals is a greater dependence on existing IFIs as major vehicles to distribute financing. There have been long standing criticisms of any moves towards shifting climate action to the purview of IFIs. One major bone of contention is that the very governance of these institutions is undemocratic, with majority shareholders from rich countries wielding disproportionate veto and policy setting power. From a climate justice perspective, this would put some of the most historically polluting countries in the driver’s seat over the disbursement of climate finance. In a positive development, the BI 2.0 seems to have partially responded to this anxiety by calling for the transformation of the governance of IFIs to make them more representative, equitable and inclusive.

Even so, the BI still doesn’t make the link to important climate and development finance discussions and decisions under the UN system. While there is a much welcome cross-reference to the SDGs in the BI proposals, there is no mention of the Paris Agreement and the modalities and principles that have already been developed under the UN climate talks, via democratic debate and cross-country consensus. There is already much frustration over the continued failure to commit adequate climate financing to the Adaptation Fund and the Green Climate Fund that were developed under the UN. The BI side steps any potential to link its own operationalization with these existing tools.

As such, there is a danger of taking energy away from modalities developed in more transparent spaces under the UN and of creating parallel financing systems that are under the purview of less democratically accountable IFIs. Additionally, current conversations under the BI don’t explicitly connect the proposed reforms to the climate debt owed to the global south by the global north. Nor do they link to agreed-upon reparative principles, such as common but differentiated responsibilities, that make a stronger moral case for grant based climate financing.

Where Next for Financial Systems Reform Towards Climate Justice?

There is much appreciation for what the BI is trying to do and the leadership of Barbados. But there is still a concern that it is being presented by some as “the” key way to solve structural problems within the financial system. The BI has carved out a pragmatic approach of working within the current system, but proposals for more transformative reforms need to be elevated in discussions. Additionally, areas where the BI falls short should be considered and debated. For example, its dependence on public finance to assume the risk for private investment and its potential to create more debt. Furthermore, it should be recognized that the BI doesn’t yet address fundamental questions regarding which institutions or processes should be used to deliver finance.

There is also a missed opportunity to link to important reforms being proposed in other democratic decision-making spaces. For instance, the Financing for Development Forum (FFD Forum), which is held under the auspices of the UN with equal opportunities for developing countries to contribute. During the 2023 FFD Forum held on the heels of the World Bank and IMF Spring meetings this April, the UN Secretary General noted that “the UN, as the only organisation with universal membership, is ready to facilitate inclusive dialogue on sovereign debt, bringing together the discussions that are happening in different forums”. Similarly, ideas elaborated under the BI for innovative taxation as a source for Loss and Damage funding could be more explicitly linked to UN-led discussions on tax justice, including the recent decision to form a UN Tax Convention.

Having said this, there is a very clear and pragmatic logic to the BI’s approach: it is unlikely that donor countries and other powerful actors will be receptive to demands for deep reforms they have resisted for decades. Just as Barbados managed to survive its economic crisis in 2018, BI-type interventions could still assist other countries in the short and medium term in the absence of a perfect reform agenda. But if this is the case, we should be clear what the BI can and can’t deliver and situate it more explicitly within broader needs for systemic reform. Any meaningful reform agenda must address why developing countries are in a tight fiscal space to begin with. This requires expanding conversations to address structural issues related to the nature of global trade and investment as well as illicit financial flows, unjust tax regimes and other root causes for economic distress in many developing countries.

There will continue to be discussions on the BI throughout this year at a variety of fora, including the Summit for a New Global Financial Pact in June, the World Bank and IMF annuals in Marrakech this October, and COP28 in Dubai in December, to name but a few. It is time to bring these conversations under one roof and address the ideas of the BI within a much broader reform agenda under the democratic decision-making authority of the UN. This is something Global South governments and civil society may call for over the next year and our ability to achieve climate justice could depend on whether they succeed.

[1] SDRs are special assets held by the International Monetary Fund (IMF) that could be used as an effective way of increasing cash-strapped countries’ quick access to money, particularly in emergencies. Currently, SDRs are allocated to countries via a quota system that is based broadly on how highly a country is ranked in the global economic system, rather than on a needs basis. As a result, richer countries received a larger share of SDRs during the pandemic even if they didn’t utilize or specifically need them. In contrast, many developing countries that desperately needed finance were not able to benefit from sufficient SDRs. There has been much discussion on re-channelling and re-directing existing SDR quotas as well as using this facility more regularly.

Related

The Future of Climate Finance: Will COP28 Further the Onward March Towards Increased Debt and Dependence on Markets?

Gaya Sriskanthan, Tetet Nera Lauron, Nadja Charaby